Cryptocurrencies have disrupted the traditional position of fiat money in the financial market. In order to prevent people from using more convenient anonymous digital assets, authorities set a compromise: central bank digital currency (CBDC). Let’s learn more about the underlying processes of such monetary systems, which regions already use them, and what is wrong with this new form of money.

What is CBDC and whether we need them

Central Bank Digital Currency (CBDC) is a financial tool built on blockchain. Its rate is usually tied to the national currency of a state.

CBDC’s ancestor is the electronic cash system Avant, introduced in 1992 by the Switzerland Bank. Its users could conduct transactions via a debit card system and replenish accounts with digital analogues of national currency. The Bank of Finland was the issuer. Three years after the launch, Avant was discontinued because it never became popular.

During the cryptocurrency boom, financial market participants revisited the Avant concept. CBDC emerged as an answer from authorities to the growing popularity of alternative financial tools. For example, crypto transactions are way faster and cheaper in comparison with traditional bank money transfers. It also should be noted that cryptocurrencies provide anonymity.

CBDCs, just like classic cryptocurrencies, leverage blockchain as an underlying technology. It provides the tools needed to build a decentralised system. Blockchain also prevents data falsifications and network breaches. Learn more about the technology and its features using our ultimate guide.

CBDC and cryptocurrency differences

1. CBDCs are issued and regulated by central banks. Let’s compare it to Bitcoin to understand the alternative. The most capitalised cryptocurrency is fully decentralised, which means there is no single command centre. This type of structure prevents the BTC network from collapsing in the event of one element’s failure in its multiple-element system.

2. CBDCs lack anonymity. Many authorities use the tool simply as a third form of national currency. The user needs an OS to conduct operations with CBDC. Local banks or the Central Bank itself provide all necessary tools, which involves a simple rule—no anonymity in the traditional financial system is welcome.

3. Limited functionality. CBDC user rules are determined by the Central Bank. Using the tool as an additional form of local currency means that users can conduct truncations with Central Bank Digital Currency only within the country’s market. You cannot send CBDC to the exchange account or even the side crypto wallet.

4. CBDCs are backed by the Central Bank. A financial watchdog also guarantees the safety of the tool. Bitcoin and similar cryptocurrencies’ values are determined by market demand. There is no ruling authority within the crypto market that can handle the risks.

5. Low volatility. The CBDC rate is tied to the national currency, such as the “heavy” US dollar, which barely fluctuates. Bitcoin, in turn, can skyrocket or fall off a cliff within 24 hours.

Note! CBDC are not the same thing as stablecoins—tokens with the rate tied to another asset, such as national currency, like the US dollar. Stablecoins are issued by private companies, not central banks. For example, the most capitalised stablecoin—Tether (USDT)—is issued by Tether Limited. It is a private company that backs tokens and guarantees their safety. In the CBDC case, all the responsibility goes to the authorities.

CBDC types

CBDCs come in two basic models: retail and wholesale. Retail CBDCs are made for daily payments within the country’s market, while wholesale CBDCs are dedicated to conducting large transactions among financial institutions.

There is no universal CBDC model on the market right now. Blockchain brings flexibility that authorities can use to build a national digital currency system in the chosen way.

CBDC building attempts

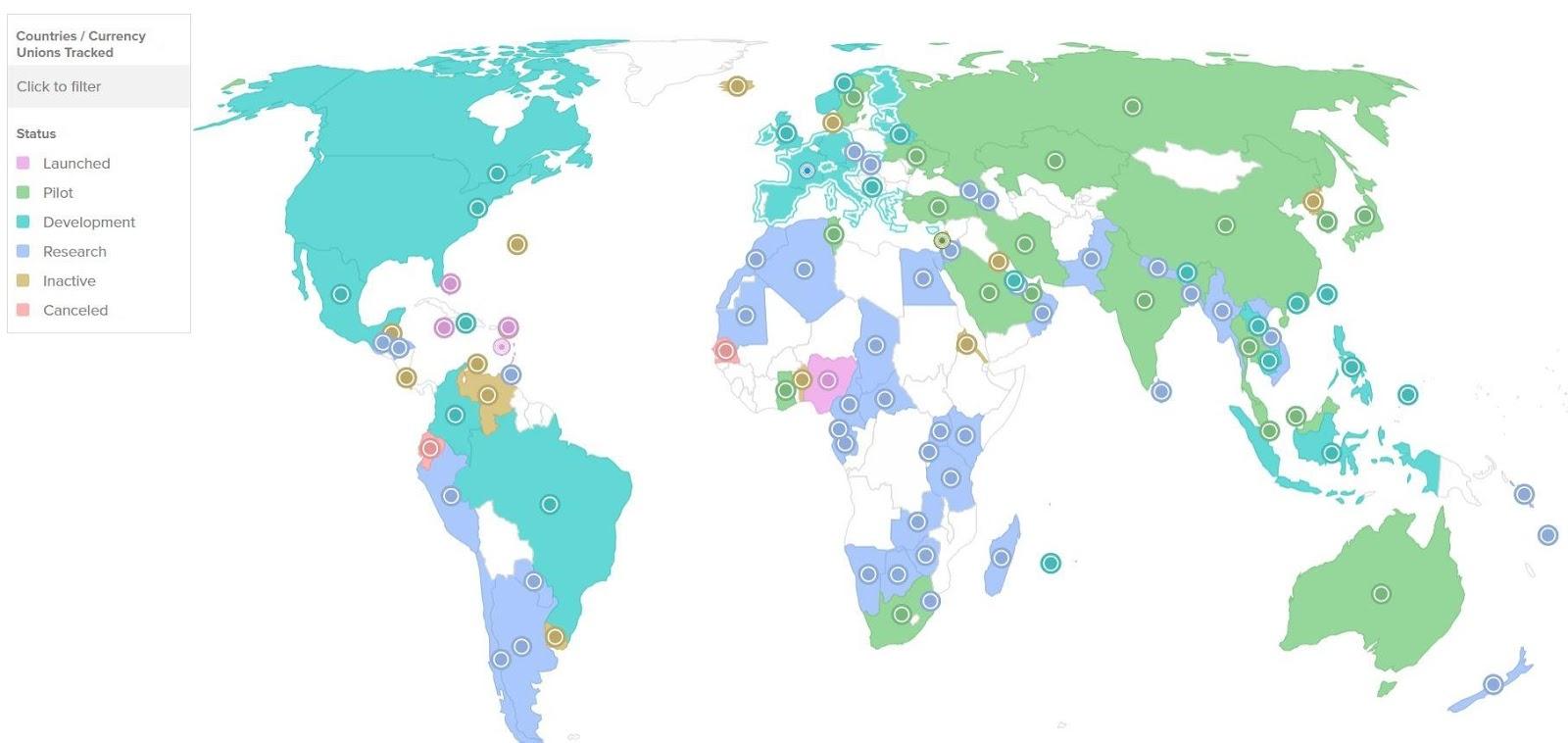

According to atlanticcouncil, CBDCs have already been launched in eleven countries: the Bahamas, Jamaica, Anguilla, Nigeria, and the Organisation of Eastern Caribbean States, which includes seven countries.

How to read the map: lilac—launched; green—pilot stage; blue—developed; light blue—research stage; brown—the CBDC project is suspended; pink—the CBDC project has been cancelled.

Bahamas CBDC. The local Central Bank Digital Currency is called the Sand Dollar. It was launched in October 2020. CBDC is dedicated to helping local citizens conduct daily payments even in non-stable electricity conditions, which is usual in the region that suffers from floods. Besides, Sand Dollar helped local authorities provide citizens in inaccessible regions with tools for making daily payments without visiting a bank. All you have to get in order to use Sand Dollar is a Central Bank-approved digital wallet.

Jamaica CBDC. Local authorities launched the Central Bank digital currency, Jam-Dex, in June 2022. The main goal of launching a CBDC is to increase financial inclusion. Any Jamaican citizen can access the Jam-Dex digital payment system. You do not need to go to the bank; just download a digital currency wallet from one of the local banks.

Organisation of Eastern Caribbean States and Anguilla CBDC. The local digital Central Bank payment system is called Dcash. It was launched in March 2021. Authorities used the project to renovate the financial system by offering users a modern tool.

Nigeria CBDC. The national digital currency, eNaira, was launched in October 2021. Local authorities used CBDC to increase the availability of digital payments in the region.

There have also been unsuccessful attempts to launch a CBDC. A striking example is Venezuela. In 2018, local watchdogs launched the Central Bank’s digital currency, Petro. Its exchange rate was tied not to the national currency but to the cost of a barrel of oil, the reserves of which, according to the authorities, are stored in the subsoil of the land under their control. With the help of Petro, the country's authorities tried to circumvent Western sanctions and fight inflation.

Unfortunately, the experiment failed. At the beginning of 2024, Venezuela “buried” its crypto project. Read more about the country’s attempts to create an “oil” CBDC in our article.

At the time of writing this review, many countries are engaged in the development of their own CBDC, including Russia, China, and the USA.

What’s wrong with CBDC

As we have learned, CBDCs are 100% controlled by central banks, which means that financial authorities are getting unlimited access to financial data, such as savings and transactions. Moreover, the issuer can freeze assets. That is why people are criticising the tool. For example, Donald Trump claims CBDC is “very dangerous” because it makes people lose their freedom.

Should we switch to CBDC?

Many countries are positioning CBDC as an alternative form of their currency. As usual, people are not forced to use a new tool.

If you are not fine with providing the Central Bank access to your financial data, there is no clear reason to abandon classic forms of fiat. At the same time, it should be noted that CBDCs are a pretty convenient tool in regions like the Caribbean if they can conduct offline transactions.

🤔 What do you think about CBDC?

Subscribe our socials to stay updated on the hottest stories about cryptocurrencies!

💌 Telegram, Twitter, Instagram, Facebook

Here are three other cool articles:

What is a spot bitcoin ETF, and why does everyone talk about it

5 most anticipated airdrops 2024

BitVM to make bitcoin smarter than altcoins

This article is not an investment recommendation. The financial transactions mentioned in the article are not a guide to action. Itez is not responsible for possible risks. The user should independently conduct an analysis on the basis of which it will be possible to draw conclusions and make decisions about making any operations with cryptocurrency.